What is a typical starter pack for any challenger bank? First of all, launch a mobile app, then issue a card, and finally… give it all for free. There is no web app in this formula. Is online service not important any more?

You can say a lot of things about neo banks: that they are fast in developing new functionalities (usually 30 updates per month vs 15 in the case of traditional banks), or that they are much worse in monetizing their clients (usually they lose 11 USD per user), or that the defining moment in their business model is to issue a metal card.

But have you ever heard about Revolut or Monzo web apps? Neither have I. Most of the leading mobile only banks were born with the promise that they will remain mobile (there are some exceptions, even Monzo has its little online banking, but we will talk about them later).

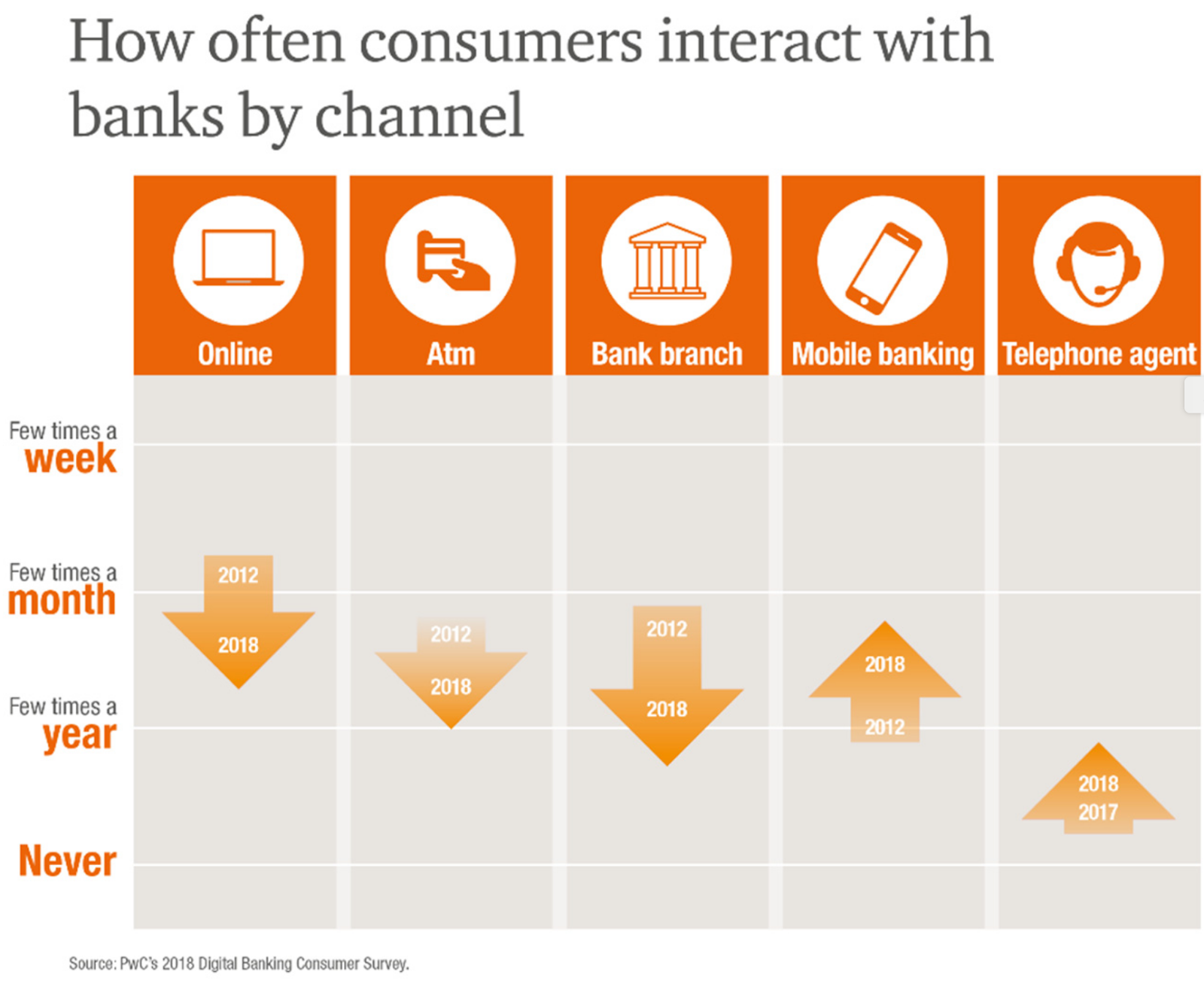

It is only a matter of 1-2 years before clients (in some countries) switch from web to mobile banking. Why?

Because the smartphone is so much more engaging.

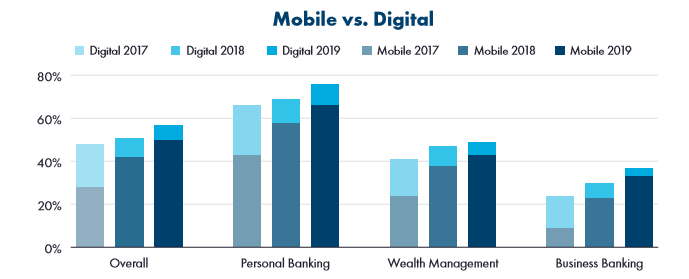

(Yes, the chart is from 2018, but the mobile trend only got stronger since then).

6 functionalities that make mobile banking better than web banking

Here are some features that make customers increasingly interact with their smartphone app:

Mobile Payments

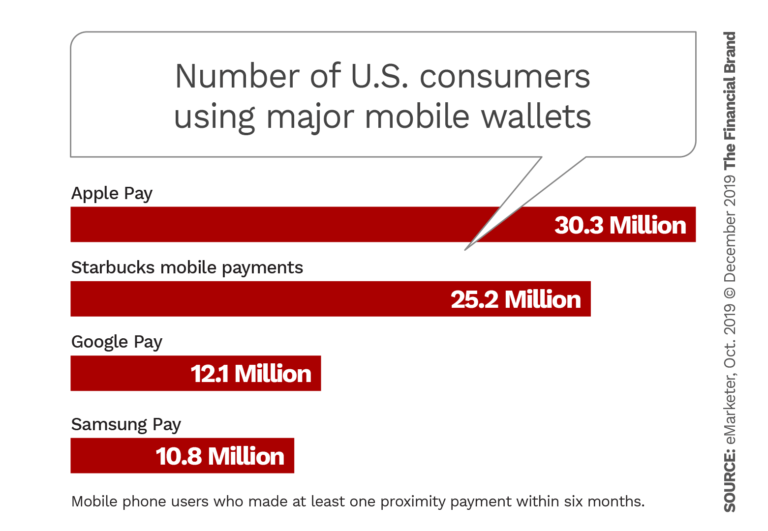

I have a friend who never took out his card of his wallet since the launch of Apple Pay. If you have a cellphone, you are able to easily pay for any goods — both offline and online. Clients can choose from a number of options, led by Google Pay and Apple Pay (or Blik if you live in Poland).

Paying in physical stores using your phone is the most MOBILE functionality you can probably imagine and will never be available through the web.

Selfie onboarding

Many banks let their customers to open an account using a selfie. when you are using a smartphone, this task is simple: you make a photo of your face and ID and that’s basically it.

But if you tried to open selfie-account on your laptop, then you know this is borderline impossible. Why? Phones have high resolution cameras, a laptop usually has a potato-quality webcam.

I tried. The web application wasn’t able to verify my face or ID due to the camera’s low resolution.

In contrast — opening an account on my mobile is a sheer pleasure.

(A camera is also helpful when it comes to invoice payments. With the OCR technology, customers of Credit Agricole can now pay invoices and bills).

Faster authorization and transactioning

Logging in to the mobile application requires the user to enter 4 digits PIN or use biometrics. It is a few times faster than in Internet banking, where first you have to enter login (usually 8 random digits) and then your password (about 12 digits). Not to mention masking mechanisms.

Mobile users have it easier when the payment authorization is considered. If your system uses SMS for authorization, then the received OTP (One Time Password) code will be filled in automatically. Also mobile tokens work like a charm.

More engagement thanks to value added services 🧳

Mobile shopping as part of the bank application is gaining popularity. At the beginning, it was only an interesting trend, but it turned out to be a useful feature which helps clients in their everyday lives.

Clients are more in control of their finances

Imagine this: you are at the counter in a grocery store. You have two shopping bags filled with milk, pasta, vegetables and other goodies. It has taken the clerk some time to scan all of them. And suddenly you get this thought: “do I have a enough money on my plastic to pay for all of that?” Have you ever been in such a situation?

It happens to me from time to time and I get a bit nervous 😬

Thanks to the mobile banking app the client can check their account balance or the transaction history at any given time or place. I found myself in a couple of situations when the funds on my card were not sufficient to pay for the shopping. I used my bank’s app to instantly top up the card with the necessary sum, paid and left the store.

Push

Mobile banking allows users to set personalized alerts – helping them stay on top of their finances by notifying them when the time to pay certain comes, or when their balances are getting low.

Why WEB banking is better than MOBILE banking?

There are couple of reasons. You can mention the bigger screen as it allows users to see more and perform more complicated tasks (like in corporate banking). Another one is that it has more functionalities then mobile. For instance — my friend’s mobile banking app doesn’t let her increase her card spending limits. The web was first on the market (and there is a saying that who hits first, hits two times) so this is a natural outcome, although the gap is gradually becoming smaller.

But from my point of view the most important reason is this:

Multi-channel means a better customer service

If you have only one door in a building and the building catches fire, what do you do? It would be wise to look for alternatives — a fire exit, fire escape ladder etc. If the bank app is down and your bank doesn’t give you access to any other contact channel, then it acts like this guy:

Offering multiple contact channels is a big advantage for banks. And this applies not only to web, but to all other channels like call center or a physical branch. Clients who have experienced troubles with solving their problems by Revolut know what I’m talking about and how important it is to have an alternative way of contacting your bank.

We can also evaluate a different scenario: what will happen If my phone gets stolen? Will I lose a way to access my account? Also, some people consider web channels to be more secure and will not try mobile banking apps.

There is one more thing — some neo banking leaders have also invested in the web channel. One of them is N26. Monzo has web, but only for emergencies: “If you’ve lost your phone, or there’s any other reason you can’t get into your Monzo app, log in here to see a stripped-back version of your account.” Revolut has a browser version of its service for the business segment.

Should traditional banks ditch their web presence?

If they are aiming at client segments that are not willing to switch to mobile, then the answer is “no”.

Should challenger banks develop web channels?

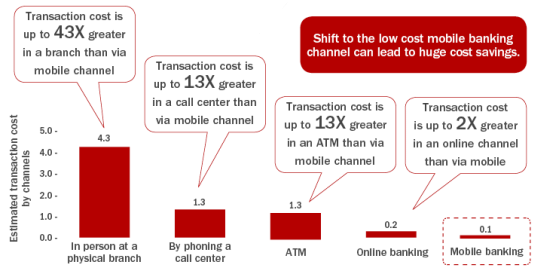

If the majority of their customers are happy with their experience, then why bother? Let’s not forget that having multi-channel presence is expensive. And that mobile is usually the cheapest.

In that scenario, banks should invest in resilient infrastructure or they may end up like Smile Bank .

Are traditional banks ready to go mobile-only?

Banks are actively preparing for mobile-only future. Over the past three years, the gap between digital and mobile in terms of capabilities has continued to shrink. Today, the two are nearly synonymous – it is unrealistic to offer a digital sales option that does not function on mobile. Today the difference in overall digital capabilities is less than 10% (probably those are the tasks that are easier to perform on a bigger screen).

Not so mobile-only future

To a growing number of consumers, banking just is a mobile activity.

According to Business Insider, 89% of the survey respondents said they use mobile banking. Furthermore, a massive 97% of millennials indicated that they use mobile banking.

Online-only customers are becoming mobile-only—and everyone else is shifting that way, too. Will there ultimately be only one banking channel? NO. New ones will emerge. But some “old” ones (like call center) will still be very useful.